Before the Tape: The Weather Case for an April Retail Beat.

The Ohio Valley just had its warmest April in 132 years. History says that matters.

Tomorrow morning at 8:30 AM EDT, the Commerce Department releases April advance retail sales. The consensus, as reflected in the Kalshi prediction market, is +0.5% month-over-month — above the historical median (and, notably, trending toward the weather signal). The macro narrative is already written: high inflation, $4.50 gasoline, negative real wages, and all-time low consumer sentiment.

Nobody is talking about the weather.

They should be.

A Record-Setting April Across the East

April 2026 was a generational warmth event across the population centers that drive spring retail. The Ohio Valley — Cincinnati, Indianapolis, Columbus, Pittsburgh, Louisville — ranked 132nd out of 132 years on record. The warmest April since 1895. The Southeast ranked 131st. The Northeast ranked 126th out of 131.

The Ohio Valley is the canary in the coal mine for April retail. Of all the regional temperature signals tested, Ohio Valley April temperature produces the strongest and most statistically significant correlation with national retail sales, significant at the 95% confidence level.

The region is the meteorological and retail fulcrum of the spring selling season: densely populated, highly indexed to weather-sensitive categories, and sitting at the geographic inflection point where spring weather variance is largest and most consequential for consumer behavior. When the Ohio Valley runs warm, the seasonal switch flips. When it runs cold, it doesn’t.

Twenty-five years of April retail sales matched against temperature records reveal a statistically significant relationship between April warmth and month-over-month retail sales growth — the percentage change from March to April, the measure that moves markets and shapes earnings narratives.

A brief note on what seasonal adjustment does — and why it matters here. The Census Bureau’s seasonal adjustment removes the predictable, recurring patterns that happen every year regardless of conditions. April is typically stronger than March for retail — consumers spend more as spring arrives. Seasonal adjustment removes that expected lift so that what remains is the true signal: did April perform better or worse than a typical April, after accounting for the calendar?

When the analysis shows warm third April years averaging +0.78% month-over-month on a seasonally adjusted basis, that means warm Aprils outperform typical Aprils even after the baseline spring lift has been stripped out. The weather effect is not simply capturing the normal March-to-April seasonal improvement. It is an additional, incremental boost on top of it. That makes the finding stronger than it first appears.

The findings:

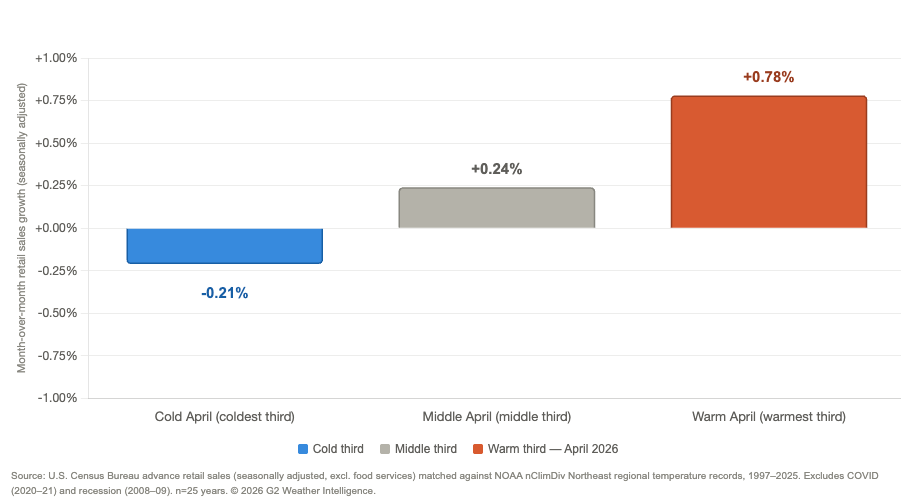

Cold Aprils (coldest third) average -0.21% month-over-month — retail sales typically decline from March

Warm Aprils (warmest third) average +0.78% month-over-month — retail sales grow meaningfully from March

The difference between a cold and warm April is nearly one full percentage point of retail sales growth

The Ohio Valley temperature correlation with April retail is statistically significant at the 95% confidence level — the strongest regional predictor of the national number in the dataset

The relationship holds even after controlling for Easter timing and prior month momentum — temperature is an independent driver of April outcomes, not just a seasonal proxy

April 2026 sits in the warmest third of all April temperature records going back to 1895. Warm third April years have historically averaged +0.78% month-over-month — nearly a full percentage point above cold third years and well above the historical April median of +0.37%. The temperature setup suggests a value above the consensus.

Two honest caveats —

First, the warm third finding is based on eight years of data in a 25-year dataset — the sample is small, and the variance is wide. This is a directional signal, not a point forecast.

Second, April 2026 is an outlier — the Ohio Valley has never been this warm in 131 years of record. The model is extrapolating beyond its training data. The true weather tailwind may be larger than the historical average suggests. Or the relationship may be non-linear at extremes. The data cannot tell us which.

What it can tell us — every April in the warm third produced better retail outcomes than the cold third average. Zero exceptions in 25 years of data.

If Thursday’s number surprises to the upside, the weather deserves a significant share of the credit. The analysts who attribute an upside surprise to consumer resilience, tax refunds, or earnings momentum will not be wrong. But they will be incomplete.

The weather was doing work that nobody on Wall Street is measuring.

The Pull-Forward Problem

March complicated the picture.

March 2026 retail sales came in at +1.90% month-over-month — one of the strongest readings in the dataset outside of COVID distortions. Three forces drove that simultaneously: historically warm March conditions, an early Easter pulling pre-holiday spending forward, and tax refunds running 11.1% above last year.

The Easter timing data is instructive. Years where Easter falls in early April — as it did this year on April 5 — historically produce flat to modestly positive April retail outcomes. The average April month-over-month in early Easter years is +0.18%. Years with strong March momentum above +1% average only +0.03% in April. The pull-forward is real and measurable in the historical record.

March 2026 likely borrowed from April. The question is how much.

The Macro Headwind

Tuesday’s CPI report quantified what consumers already felt. April inflation ran at 3.8% annually — the highest since May 2023. Gasoline averaged $4.50 nationally, up 28.4% year over year. Real wages fell 0.5% for the month. For the first time in three years, inflation ate all wage gains.

The tariff impact is showing up in the data. Apparel prices rose 0.6% in April. Household furnishings and operations up 0.7%. Airline fares up 2.8%. The categories most exposed to tariffs are the same categories that benefit most from warm spring weather.

That’s the collision Thursday’s number will reveal.

The Tiebreaker

Three forces in the ring simultaneously.

The weather signal says above consensus — warm third April years average +0.78% month-over-month and April 2026 ranks in the warmest positions on record across the East.

The Easter pull-forward says below consensus — strong March years average only +0.03% in April and early Easter years average +0.18%.

The macro headwind says downside risk — record inflation, negative real wages, and $4.50 gasoline represent the most severe combination of headwinds seen alongside record warmth in the historical dataset.

The Kalshi prediction market has moved to +0.5% — above the historical median of +0.37% and closing in on the weather signal. That's the market's best estimate of where these forces net out. Someone is buying the upside.

Something has to give. Thursday tells us which signal won.

What to Watch

The headline number will get the macro narrative. Watch the category breakdown for the weather signal:

Building materials and garden equipment — the most direct read on whether historically warm April temperatures activated outdoor project demand despite macro headwinds. A strong number here is weather. A weak number suggests macro overrode the temperature signal.

Clothing and accessories — tariffs pushed apparel prices up 0.6% in April. Unit volumes may have softened even if dollar sales held. Watch for this in the earnings calls that follow.

Nonstore retailers — online has been the consistent outperformer. Up 10.1% year-over-year in March. Watch whether that momentum held as consumers traded down from in-store to online to manage budgets.

Restaurants and food service — warm temperatures historically drive restaurant traffic. But $4.50 gasoline and negative real wages push consumers toward eating at home. The April restaurant number is the early read on Memorial Day demand.

The G2 Weather Intelligence Read

April 2026 gave consumers every meteorological reason to spend on spring categories. The Ohio Valley ran warmer than any April in 132 years. The Northeast ran warmer than 95% of Aprils on record. The weather setup was generational.

Whether that signal was strong enough to overcome $4.50 gasoline, record inflation, and negative real wages is the question Thursday answers.

The consensus has moved to +0.5% — above the historical median and closing in on the weather signal. The macro says below. If the number beats consensus — you heard the weather argument here first.

The Weather-Ready Consumer Enterprise — a new Friday Brainstorm Series from G2 Weather Intelligence — launched last week on Substack. How retail, CPG, and healthcare executives can build weather intelligence into every major decision-making workflow. New posts every Friday. Free for the first seven days — subscribe at www.g2weather.com to get each post delivered to your inbox before it goes behind the paywall.

© 2026 G2 Weather Intelligence. All rights reserved. If you reference or quote this analysis, please attribute it to G2 Weather Intelligence and include a link to the original post. For media inquiries, contact paul.walsh@g2weather.com