G2 Weather Signal™ Flash Report — Jan 19, 2026

Winter Is Coming! Extreme Cold Shifts the Weather Signal From Noise to Earnings Risk

“Polar Vortex Hammer drops on Midwest and Great Lakes into next weekend with brutal cold + ice storm potential in Texas to Southeast.” —Dr. Ryan Maue

Signal Summary

Arctic cold arrives forcefully, shifting demand toward urgency-driven categories (auto parts, consumables, emergency repair) while pressuring traffic-dependent retail and restaurants.

This week reallocates demand, not lifts it: necessity wins (AutoZone, Walmart, Lowe’s), while cold suppresses mobility and visit frequency for brands like Starbucks, Chipotle, and TJX.

Next week is the margin test as cold broadens into the Midwest, Ohio Valley, and Northeast, exposing inventory imbalance and execution risk more than driving incremental sales.

February marks a rotation, not relief: early spring warmth in the South and California benefits routine-driven models, while winter urgency fades unevenly, rewarding discipline over exposure.

Winter is coming?

Damn right!

For the purist weather geeks who are already tsk-tsk’ing me (yes, winter officially began on December 21 — we know), I’m not talking about just any winter.

I’m talking about the kind of winter that many of those same purists — or “aficionados,” as we used to call them back in my Weather Channel days — have never actually experienced.

Which brings me to Dr. Maue’s headline from last night:

Here comes the worst/coldest winter weather since the 1970s.

We’re staring at an almost worst-case cold setup for North America as we head deeper into late January: a deeply frigid Arctic air mass plunging south out of Canada, with a boost from Siberia.

This won’t be a one-off cold snap. It’s shaping up as a long-duration extreme cold event, arriving in two major waves — one this coming weekend, and another shortly after. Even before those main blasts arrive, the upcoming week turns sharply colder across the Midwest and Great Lakes, keeping the Lake Effect snow machine running at full throttle.

For retailers, restaurants, and CPG companies, this kind of cold leaves a mark — and it’s a central theme in today’s Flash report.

A note to subscribers:

As I continue to evolve the weekly product, I’m refining how content is split between the free and premium tiers. Starting today:

Free subscribers receive the top five and bottom five weather-driven names for last week and this week, ranked by the G2 Weather Exposure Index, along with the current-week forecast.

Premium subscribers receive top/bottom five forecast exposure indices across all forward horizons, including the 2–4 week outlook and the month-ahead forecast.

Let’s get into it.

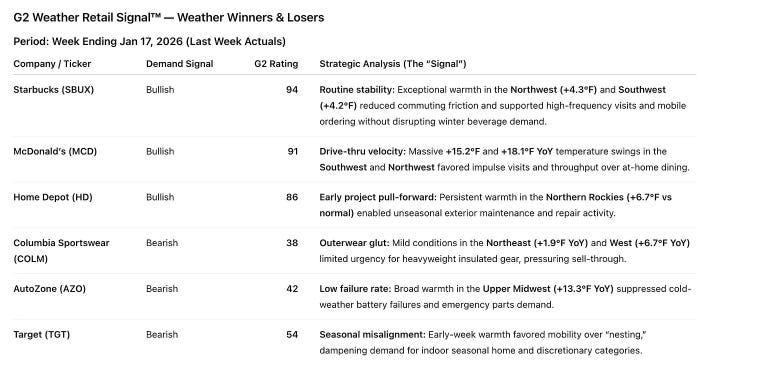

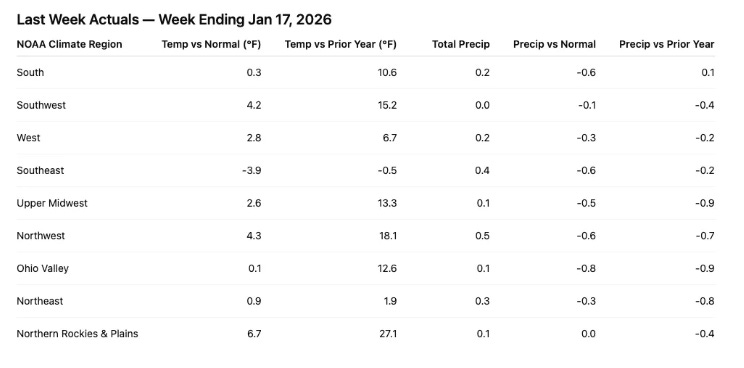

Last Week (Week Ending Jan 17, 2026)

Residual Warmth, Minimal Activation

Last week closed with above-normal temperatures across most regions, including the South, West, Southwest, and Northern Rockies & Plains. Year-over-year comparisons were even warmer, particularly in the Upper Midwest, Northwest, and Northern Rockies.

That warmth limited winter urgency nationally. While conditions were seasonally acceptable in the Northeast, they were not cold enough — nor widespread enough — to drive full-price winter activation.

Precipitation remained generally light and below normal across most regions, reducing disruption but also offering little incremental demand catalyst.

Bottom line: mostly benign weather nationally, low activation, limited earnings relevance.

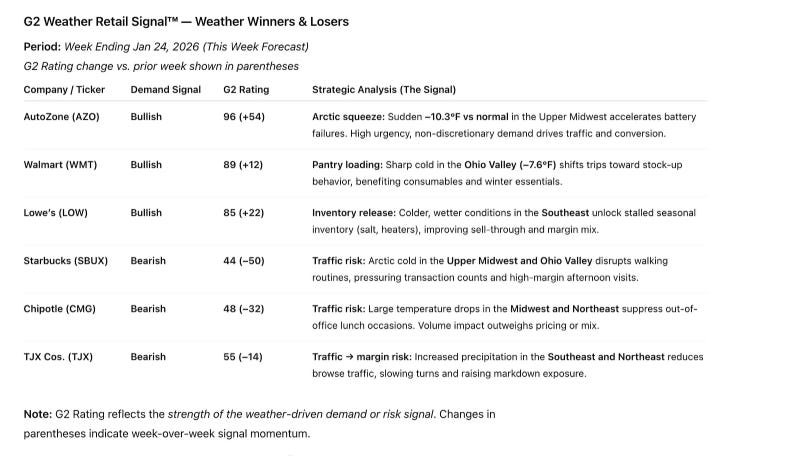

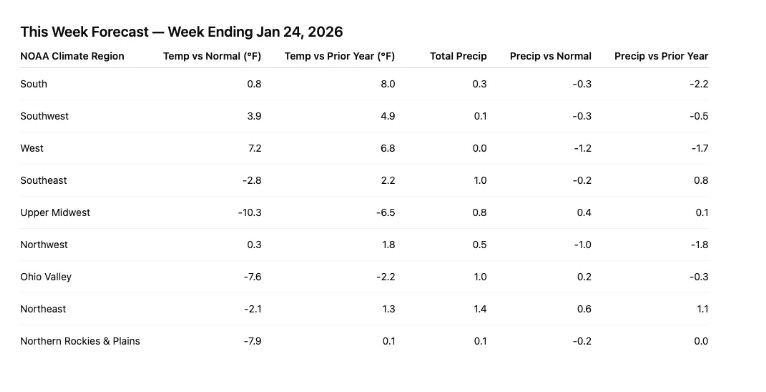

This Week (Week Ending Jan 24, 2026):

Arctic Cold Reshapes Retail— Necessity Wins, Traffic-Driven Models Lose

This week’s Arctic-driven divergence produces clear winners and losers across retail and restaurants, as extreme cold collides with uneven regional execution.

On the beneficiary side, the Exposure Index flags AutoZone (AZO) as the clearest winner. The sudden Arctic plunge in the Upper Midwest creates a textbook battery-failure environment — high urgency, non-discretionary demand, and strong conversion.

Walmart (WMT) also screens positively, as sharp cold in the Ohio Valley drives pantry loading and winter essentials stock-up behavior. Lowe’s (LOW) benefits more selectively, with colder, wetter conditions in the Southeast finally unlocking stalled winter seasonal inventory and improving clearance efficiency.

The pressure points, however, skew heavily toward traffic-dependent restaurant and discretionary retail models.

Starbucks (SBUX) and Chipotle (CMG) sit on the wrong side of the Exposure Index this week. Arctic cold in the Upper Midwest and Ohio Valley disrupts walking and short-trip routines, suppressing high-frequency visits and eroding transaction counts faster than tickets can make up for it.

TJX Companies (TJX) faces a different risk profile: increased precipitation across the Southeast and Northeast reduces browse-driven traffic, slowing turns and raising markdown exposure just as winter inventory remains elevated.

This weather doesn’t lift retail broadly. It reallocates demand toward urgency and away from discretionary, traffic-dependent formats.