The Blue on This Map is Worth Millions in Lost Summer Sales

Last June was one for the record books. This June the bill is coming due.

"God created economists to make weather forecasters look good."

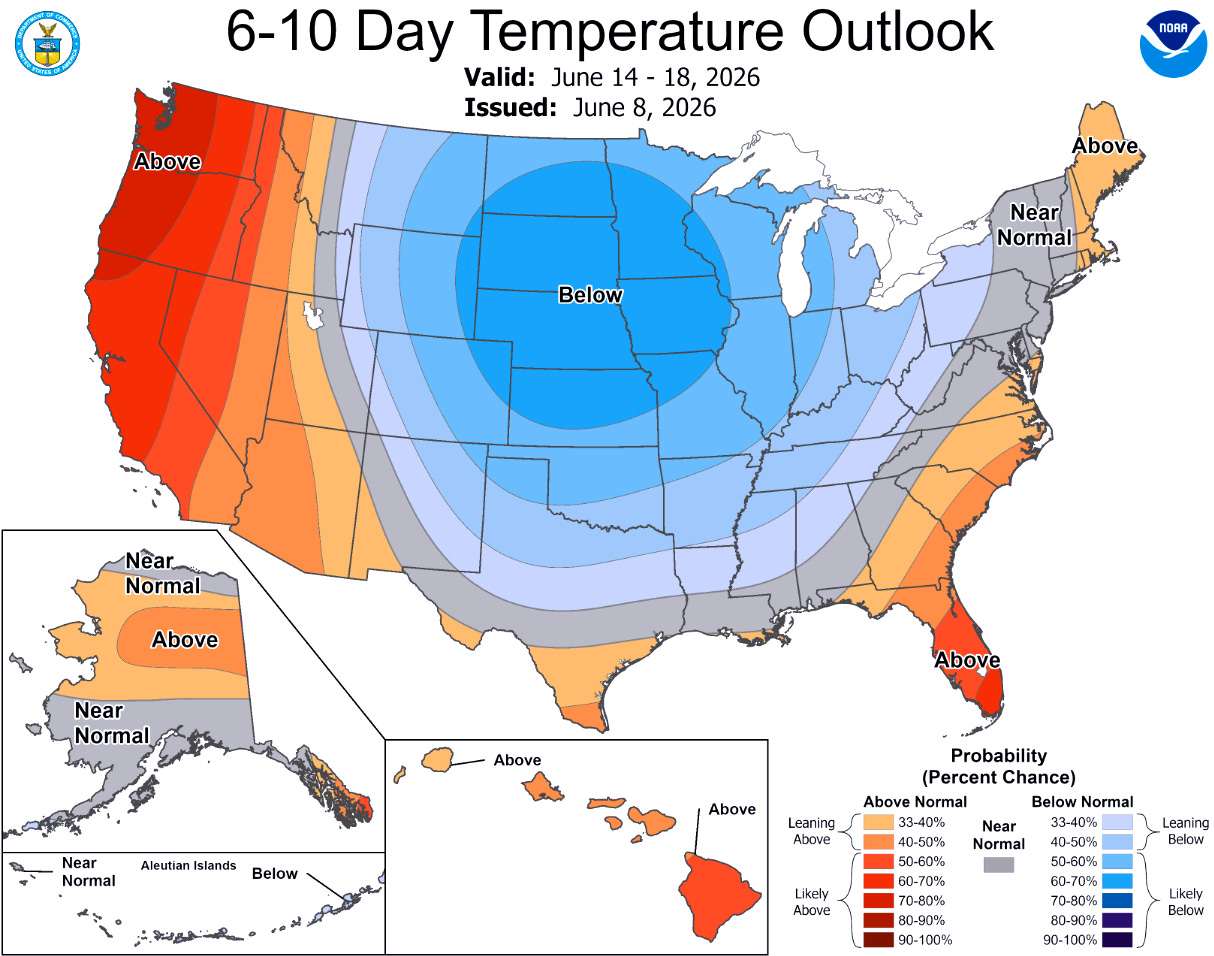

The most accurate forward-looking signal available to any retailer with seasonal categories isn't on Wall Street. It's at NOAA. And the latest outlook is unambiguous.

The updated 6-10 day outlook issued June 8 shows a deep below-normal temperature pool dominating the Central and Eastern US through June 14-18 — blue from the Rockies to the Mid-Atlantic. Above-normal precipitation across the South and Southeast.

{kind=link}