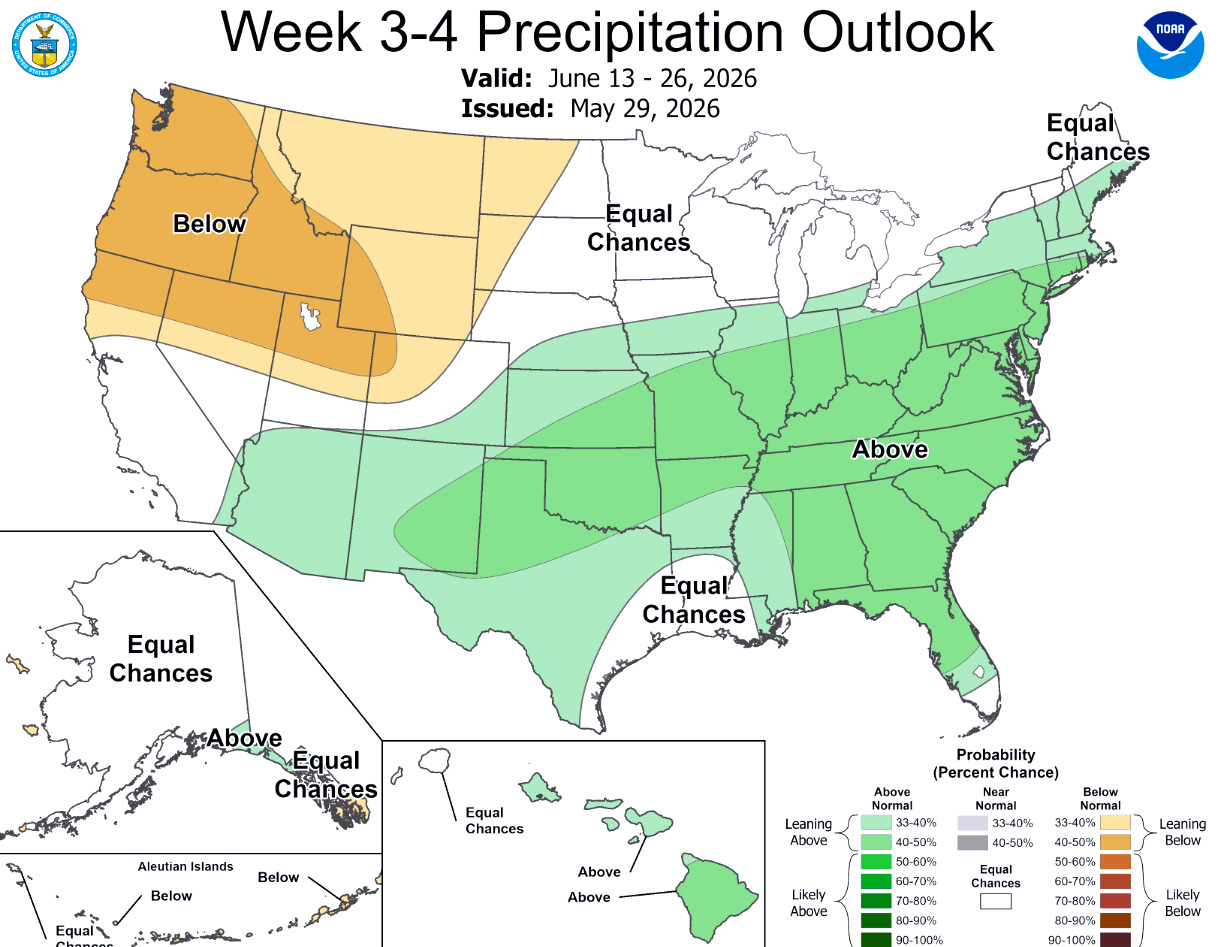

The Tailwinds Are Gone. The Headwinds Are Real.

G2 Weather Weekly | June 13 – June 26, 2026 | Paul Walsh

“It’s a hard rain’s a-gonna fall” —Bob Dylan

CNBC’s retail roundup this week called Q1 “surprisingly robust” and correctly identified three tailwinds that buoyed results — tax refunds, buy now pay later, and consumer resilience.

What it missed? The weather.

February through April 2026 was one of the warmest springs in more than 130 years. The national temperature ran more than 5 degrees above normal for the entire window.

{kind=link}